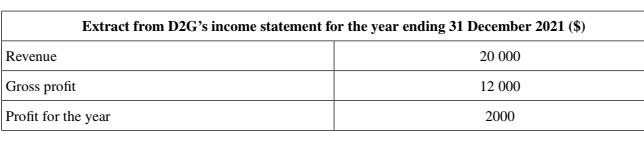

D2G is a driving school. Mattan started D2G 3 years ago to teach people to drive a car. As the business has been successful Mattan plans to buy a new vehicle. He has been analysing D2G’s income statement. An extract is shown in the table below. Mattan wants to understand the difference between profit and cash. He also wants to know how an increase in competition and changes in the business cycle might affect D2G.

- extract from d2g.JPG (16.37 KiB) Viewed 208 times

11 Outline, with reference to D2G, the difference between profit and cash. [4]

Possible KN Points:

• Cash is needed to pay day-to-day costs

• whereas profit is necessary for the long-term survival

• Cash may be received beforehand

• will not increase until later

• D2G may offer credit to a clear reference to the customers

• but the cash is not yet received

• Profit is a source of finance

• Profit is a measure of success

• Profit is a reward for risk-taking

• Cash is necessary to help avoid cash flow problems